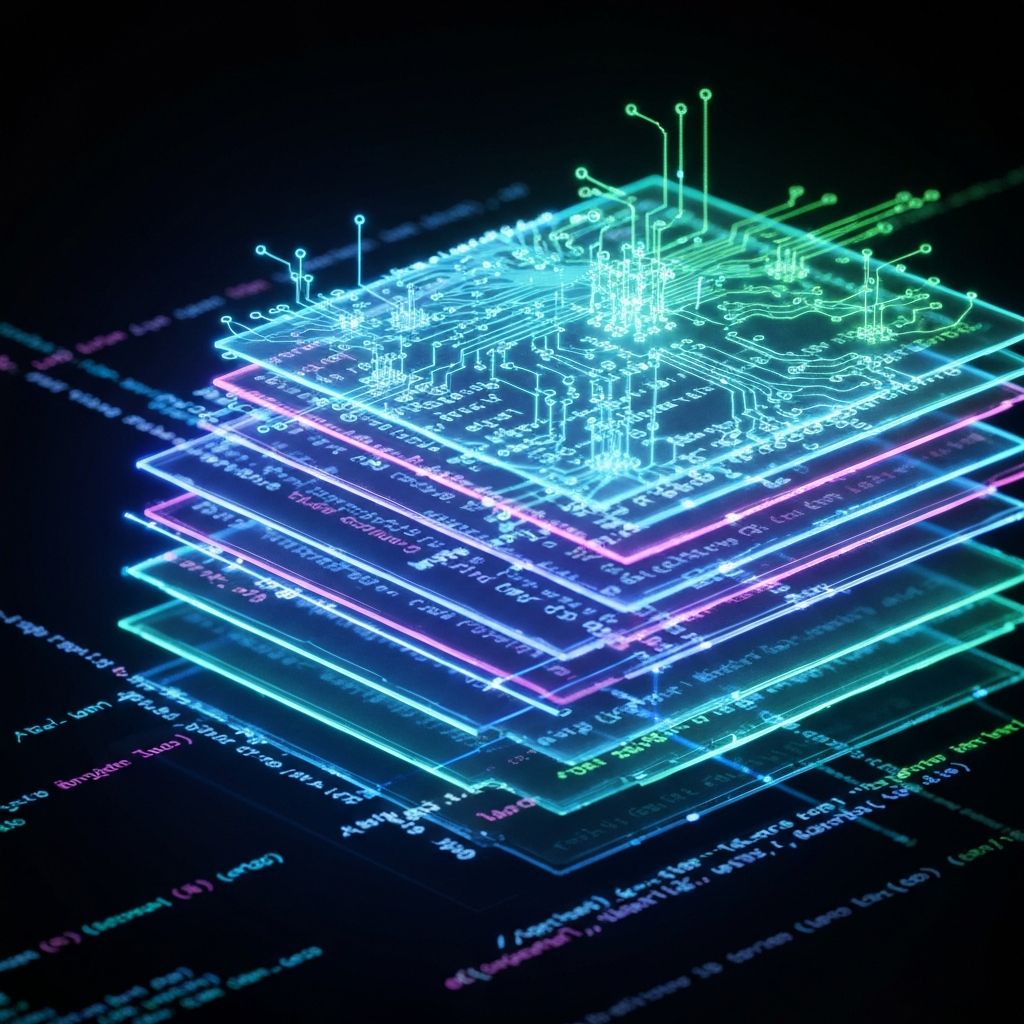

QFabric: 5-LayerSoftware Architecture

A comprehensive quantum-classical hybrid platform designed specifically for financial workloads, delivering sub-microsecond latency and 40x performance improvements over classical Monte Carlo methods.

Explore LayersFull-Stack Quantum Integration

QFabric provides a complete abstraction from application interface to hardware control, enabling seamless execution across custom QPUs and third-party quantum backends.

Application Interface Layer

High-level abstraction providing financial institutions with pre-built algorithm templates and circuit builders optimized for risk, portfolio optimization, and options pricing workloads.

Intermediate Representation Layer

Proprietary IR extended from OpenQASM 3.0, featuring financial-specific primitives and real-time classical control for hybrid quantum-classical algorithms.

Compilation & Optimization Engine

Advanced transpiler with intelligent pass management, automatically optimizing circuits for target hardware topology while implementing error mitigation strategies.

Backend Abstraction Layer

Unified interface for heterogeneous quantum backends, providing seamless job scheduling, credential management, and sub-microsecond dispatch to both custom and third-party hardware.

Hardware Control Layer

Direct FPGA pulse control with RFSoC integration, enabling real-time waveform generation and feedback for QuantaBull's custom QPU and classical accelerators.

Complete Risk Calculation Pipeline

End-to-end workflow demonstrating how QFabric processes financial risk calculations from data ingestion to result delivery.

Data Ingestion

Market data, portfolio positions, and risk parameters loaded via REST API or WebSocket

Circuit Generation

Quantum circuits auto-generated from algorithm templates and compiled for hardware

Quantum Execution

Circuit executed on custom QPU with real-time error mitigation and adaptive feedback

Results & Analytics

VaR, CVaR, Greeks, and sensitivity metrics delivered via API with confidence intervals